Introduction

Health is wealth — and in 2025, securing affordable and reliable health insurance has never been more important. Rising medical costs, unpredictable emergencies, and increasing awareness about preventive care have made health insurance a necessity rather than a choice.

Whether you’re an individual seeking basic coverage, a family needing comprehensive protection, or an employee evaluating employer-sponsored benefits, the right health insurance plan can save you thousands of dollars annually.

With numerous providers and plan types available, choosing the best one isn’t always easy. This guide covers the top health insurance plans in 2025, including UnitedHealthcare, Kaiser Permanente, Blue Cross Blue Shield, Aetna, and Cigna. You’ll learn how to compare plans, maximize coverage, and save money.

What Is Health Insurance?

Health insurance is a financial agreement between you and an insurance company. You pay a monthly premium, and in return, the insurer helps cover medical expenses such as doctor visits, hospital stays, surgeries, medications, and preventive care.

Why It Matters in 2025

- Rising Healthcare Costs: Medical inflation continues, making out-of-pocket payments risky.

- Unexpected Emergencies: Accidents or sudden illnesses can cost thousands without insurance.

- Preventive Care: Modern plans cover screenings, vaccinations, and wellness visits for free.

- Peace of Mind: Insurance reduces stress by protecting both health and finances.

Key Features to Look for in a Health Insurance Plan

Not all insurance plans are created equal. Consider these features when evaluating coverage:

1. Premiums

The amount you pay monthly for coverage. Lower premiums may have higher deductibles, while higher premiums usually include better coverage.

2. Deductibles

The amount you pay out-of-pocket before insurance begins covering costs. Plans with higher deductibles often have lower monthly premiums.

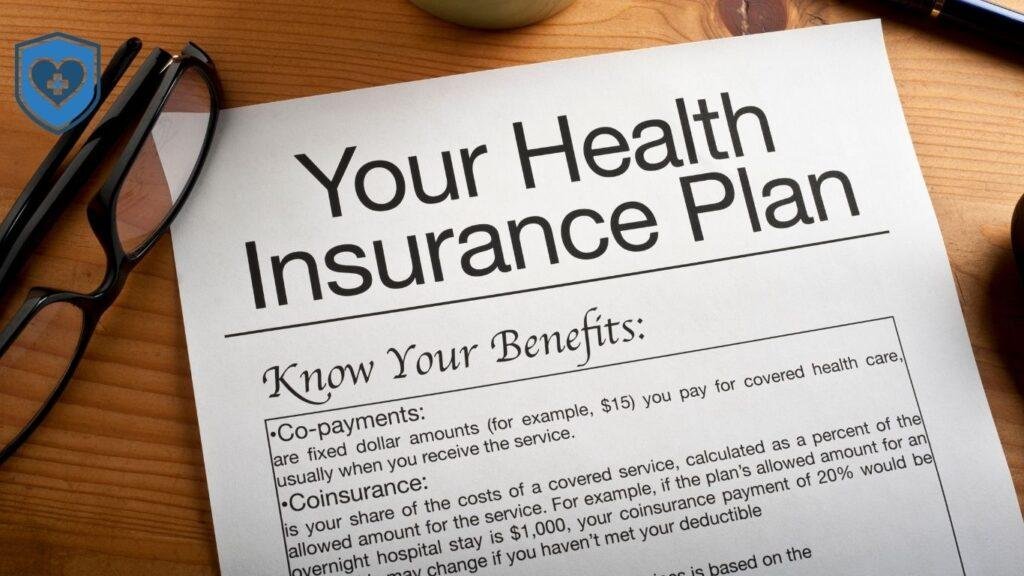

3. Co-Payments & Co-Insurance

- Co-pay: A fixed fee per doctor visit (e.g., $20).

- Co-insurance: A percentage you pay after meeting your deductible (e.g., 20%).

4. Network of Doctors and Hospitals

Some providers limit coverage to in-network doctors. UnitedHealthcare, for example, has one of the largest provider networks in the U.S., ensuring wide access to hospitals and specialists.

5. Prescription Drug Coverage

Check whether your medications are included and the tiers (generic, preferred, non-preferred).

6. Preventive & Wellness Benefits

Most modern plans cover screenings, vaccines, and wellness programs — crucial for maintaining long-term health.

7. Additional Benefits in 2025

- Telehealth & Virtual Visits: Remote care included in most plans.

- Mental Health Services: Coverage for therapy and counseling.

- Maternity & Family Planning: Essential for young families.

- Chronic Disease Management: Support for conditions like diabetes and hypertension.

Types of Health Insurance Plans in 2025

Understanding plan types helps you select the right coverage for your needs.

1. Health Maintenance Organization (HMO)

- Requires using in-network providers.

- Requires a primary care physician (PCP) referral for specialists.

- Usually lower premiums and out-of-pocket costs.

2. Preferred Provider Organization (PPO)

- Allows visits to out-of-network doctors at higher costs.

- No referral needed for specialists.

- Greater flexibility but slightly higher premiums.

3. Exclusive Provider Organization (EPO)

- Must use in-network providers.

- No referrals needed.

- Balances cost and flexibility.

4. Point of Service (POS)

- Requires a PCP referral for specialists.

- Can see out-of-network providers at a higher cost.

- Hybrid between HMO and PPO.

5. Government-Sponsored Plans

- Medicare: For individuals 65+ or with disabilities.

- Medicaid: Income-based coverage for eligible low-income individuals and families.

6. Short-Term Health Insurance

- Temporary coverage for gaps between plans.

- Usually limited in coverage for pre-existing conditions.

Best Affordable Health Insurance Providers in 2025

Here’s a comparison of the top providers offering reliable and affordable health insurance options:

| Provider | Plan Type | Monthly Premium | Deductible | Network Coverage | Key Features |

|---|---|---|---|---|---|

| UnitedHealthcare | PPO/HMO | $350–$500 | $1,500 | Nationwide | Telehealth, wellness programs, large provider network |

| Kaiser Permanente | HMO | $300–$450 | $1,200 | Regional (West Coast) | Integrated care, online services, preventive care focus |

| Blue Cross Blue Shield | PPO/EPO | $400–$550 | $1,500 | Nationwide | Flexible networks, prescription coverage, 24/7 nurse line |

| Aetna | HMO/PPO | $320–$480 | $1,400 | Nationwide | Virtual care, mental health programs, wellness discounts |

| Cigna | PPO/HMO | $350–$500 | $1,350 | Nationwide | Chronic condition management, telemedicine, preventive care |

Tip: Premiums vary based on age, location, plan tier, and employer contributions. Always compare plans based on total cost (premium + deductible + co-pays).

How to Choose the Right Health Insurance Plan

Selecting the right plan depends on personal factors:

- Assess Your Health Needs – Consider ongoing medications, chronic conditions, or planned procedures.

- Budget for Premiums and Out-of-Pocket Costs – Balance affordable monthly payments with deductibles.

- Check Provider Networks – Ensure your preferred doctors and hospitals are included.

- Review Coverage Details – Pay attention to preventive care, maternity, mental health, and telehealth benefits.

- Consider Family Needs – Evaluate coverage for spouses and children if applicable.

Pros & Cons of Health Insurance in 2025

Pros

- Financial protection against high medical costs

- Access to preventive care and wellness programs

- Peace of mind for emergencies

- Discounts on medications and telehealth services

Cons

- Monthly premiums may be expensive for some

- Out-of-pocket costs for certain procedures

- Some plans restrict coverage to in-network providers

Tips for Saving Money on Health Insurance Premiums

- Use Government Subsidies: Check eligibility for ACA marketplace tax credits.

- Compare Multiple Providers: Don’t settle for the first quote.

- Opt for Higher Deductibles: Lower premiums can save money if you’re healthy.

- Leverage Employer Benefits: Employer-sponsored plans often include contributions.

- Stay Healthy: Participate in wellness programs to reduce premiums and qualify for discounts.

Frequently Asked Questions (FAQ)

Q1: What is the cheapest health insurance in 2025?

A1: Short-term plans or Medicaid for eligible individuals can be cheapest, but coverage may be limited. Always consider total cost, not just monthly premiums.

Q2: Is it better to choose private insurance or employer insurance?

A2: Employer-sponsored plans often provide better value due to employer contributions, but private plans offer flexibility in choosing doctors.

Q3: Do health insurance plans cover pre-existing conditions in 2025?

A3: Most ACA-compliant plans, including UnitedHealthcare and Blue Cross Blue Shield, cover pre-existing conditions without extra charges.

Q4: Can I use telehealth services with my insurance plan?

A4: Yes, most top providers like Aetna, Cigna, and Kaiser include telehealth visits at low or no cost.

Conclusion

Finding the best health insurance plan in 2025 requires research, comparison, and understanding your personal and family health needs. Providers like UnitedHealthcare, Kaiser Permanente, Blue Cross Blue Shield, Aetna, and Cigna offer reliable coverage with varying premiums and benefits.

Focus on plans that balance affordability, comprehensive coverage, and additional perks like telehealth, preventive care, and wellness programs. By choosing wisely, you can protect your health, secure your finances, and gain peace of mind in 2025.

Pro Tip: Reassess your plan annually — medical needs, premiums, and network options may change. Staying informed ensures you always have the best affordable health insurance coverage.